Resumen ejecutivo

Cuando se trata de adquirir un casino en línea, una red de afiliados de juegos de azar o cualquier activo relacionado con los juegos en línea, uno de los mecanismos de financiación más pragmáticos —y a menudo infrautilizados— es la financiación del vendedor, que suele formalizarse mediante lo que en el sector se denomina un «pagaré del vendedor». A diferencia de los préstamos bancarios convencionales o las estructuras de financiación de la SBA, un pagaré del vendedor se gestiona directamente entre el comprador y el vendedor, lo que facilita su ejecución, ofrece mayor flexibilidad en sus términos y resulta especialmente adecuado al perfil de riesgo único de los activos de juegos en línea.

de pequeña y mediana capitalización las ventas de negocios de iGaming —más del 80 %— incluyen algún tipo de financiación por parte del vendedor. En el caso específico de las adquisiciones de casinos online en el mercado medio, el préstamo del vendedor suele representar entre el 10 % y el 30 % del valor total de la transacción. Esta estructura beneficia a ambas partes: los vendedores pueden obtener valoraciones más altas y disfrutar de ingresos a plazos con ventajas fiscales, mientras que los compradores acceden a operaciones de iGaming consolidadas sin necesidad de desembolsar el capital completo por adelantado.

Ya sea que esté vendiendo un casino en línea con licencia, un sitio afiliado a un casino con ingresos establecidos vinculados a GGR o una plataforma de iGaming de marca blanca, esta guía de CasinosBroker.com aborda todas las dimensiones de la financiación del vendedor que necesita comprender antes de iniciar las negociaciones.

1. ¿Qué es la financiación del vendedor en las fusiones y adquisiciones de empresas de juegos en línea?

La financiación por parte del vendedor —también conocida como pagaré del vendedor, contraprestación diferida o nota del vendedor— es una estructura de transacción en la que el vendedor de un negocio acepta una parte del precio de compra en cuotas durante un período acordado, en lugar de exigir el pago total al cierre. El comprador realiza un pago inicial al momento de la adquisición y luego paga el saldo restante mediante cuotas mensuales regulares, más intereses, hasta que el pagaré se haya liquidado por completo.

Para ilustrarlo: si un casino online regulado se cotiza a 5.000.000 € y el vendedor acepta financiar el 40 % del precio de compra, el comprador paga 3.000.000 € al cierre de la operación y luego devuelve los 2.000.000 € restantes en un plazo de, digamos, cinco años, con un tipo de interés acordado. Esta es una práctica habitual en las fusiones y adquisiciones en el sector del iGaming, y en CasinosBroker.com, estructuramos y asesoramos sobre este tipo de acuerdos con regularidad.

Dado que los activos de iGaming —ya sean casinos con licencia, casas de apuestas deportivas, salas de póker o sitios web de afiliados con mucho tráfico— suelen ser difíciles de valorar con los modelos bancarios convencionales, la financiación del vendedor resuelve este problema. Los bancos rara vez conceden préstamos con garantía del fondo de comercio o la base de datos de jugadores de las empresas de iGaming. Por lo tanto, los vendedores que ofrecen financiación estructurada acceden a un grupo mucho mayor de compradores cualificados.

2. ¿Por qué la financiación por parte del vendedor domina las estructuras de acuerdos en el sector del iGaming?

La industria del iGaming opera en un entorno regulatorio complejo, con un alto nivel de licencias y particularidades jurisdiccionales, que las instituciones financieras tradicionales tienen dificultades para financiar. Un negocio físico con activos tangibles es una cosa; un casino en línea con licencia de Malta, cuyo valor principal reside en su base de datos de jugadores, infraestructura de bonos, brutos del juego y relaciones con afiliados, es algo completamente distinto. La mayoría de los bancos simplemente no otorgan financiamiento para la adquisición de este tipo de activos.

Aquí es donde la financiación del vendedor se convierte no solo en una opción, sino a menudo en la única vía viable para cerrar la adquisición de una empresa de juegos en línea. Es más rápida de gestionar que la financiación bancaria, requiere mucho menos papeleo y suele ofrecer condiciones más flexibles, adaptadas a la situación económica real del negocio adquirido. Además, existen ventajas importantes para el vendedor:

La eficiencia fiscal es una gran ventaja. Dado que los vendedores solo pagan impuestos sobre las ganancias a medida que las reciben —y no en un pago único al cierre de la operación—, un pagaré a plazos bien estructurado puede distribuir la obligación tributaria de manera significativa a lo largo de varios ejercicios fiscales. Para transacciones de casinos de alto valor, esto puede traducirse en ahorros sustanciales.

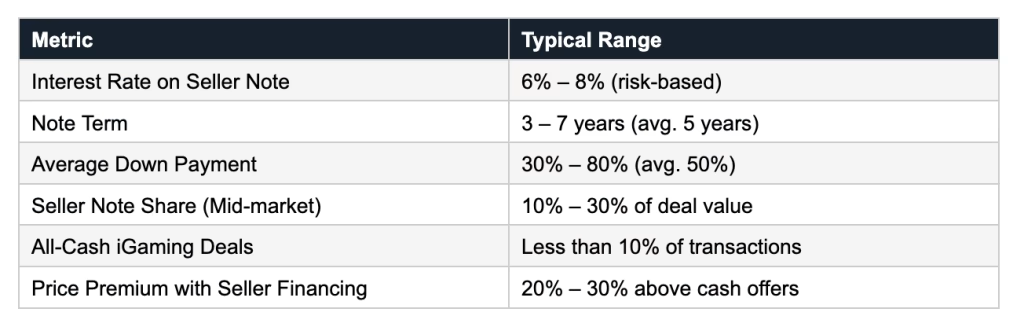

Los vendedores que ofrecen financiación suelen obtener precios de compra más elevados. Según datos agregados de miles de transacciones de compraventa de empresas, las empresas vendidas con financiación del vendedor alcanzan valoraciones entre un 20 % y un 30 % superiores a las de activos similares vendidos al contado. En el sector del iGaming, esta prima refleja la continua confianza del vendedor en el activo y su disposición a mantener su compromiso financiero con su éxito tras la adquisición.

Por último, los activos de iGaming con financiación del vendedor se venden más rápido. La rapidez es crucial en este sector: las licencias regulatorias tienen plazos de renovación, los contratos de afiliación se prolongan indefinidamente y las bases de datos de jugadores se deterioran si se dejan en un limbo operativo. Un pagaré del vendedor bien estructurado agiliza las transacciones y reduce el tiempo entre la carta de intención y la formalización de la venta.

3. Cómo protegerse como vendedor: Diligencia debida y seguridad

En el momento en que usted acepta actuar como prestamista en su propia transacción, hereda las obligaciones de un prestamista, incluida la responsabilidad de calificar adecuadamente a su comprador. En CasinosBroker.com, recomendamos a los vendedores que califiquen al comprador con el mismo rigor que aplicaría un banco comercial. Esto implica recopilar un estado financiero detallado, un informe de crédito personal o corporativo, una biografía profesional o un historial operativo, y cualquier historial relevante de licencias de iGaming que el comprador pueda tener.

Para los compradores corporativos —en particular, sociedades holding, vehículos de capital privado u operadores estratégicos que buscan expandir su cartera de casinos en línea— los vendedores deben solicitar documentación sobre las adquisiciones previas del comprador, referencias de vendedores anteriores y evidencia de su desempeño operativo posterior a la adquisición. Un comprador que no pueda demostrar que ha integrado y desarrollado con éxito un activo de juegos en línea debe ser examinado minuciosamente antes de que usted acepte financiar cualquier parte de la venta.

En nuestra experiencia, la causa más común de impago por parte del vendedor es un pago inicial insuficiente. Consideramos que cualquier pago inicial inferior al 30 % del precio de compra acordado representa un riesgo significativo. Nuestra recomendación habitual es exigir un pago inicial mínimo del 30 % al 50 %, y tratar los importes inferiores como una señal de alerta en la negociación, en lugar de una concesión que se pueda aceptar. Un comprador que aporta un capital considerable tiene un interés real en la operación y un incentivo genuino para cumplir con el pago.

Además del pago inicial, los vendedores deben exigir informes financieros posteriores al cierre —como mínimo, estados de pérdidas y ganancias mensuales o trimestrales y estados de ingresos brutos del juego (GGR)— y pueden negociar cláusulas basadas en hitos, vinculadas a niveles mínimos de ingresos netos del juego (NGR), número de jugadores activos o niveles mínimos de capital de trabajo. Esto es especialmente relevante en las adquisiciones de casinos en línea, donde los ingresos pueden ser volátiles y muy sensibles a los cambios en la estrategia de bonos, las relaciones con los proveedores de pago o la combinación de fuentes de tráfico.

En los casos en que los antecedentes del comprador justifiquen un escrutinio más exhaustivo —o cuando el pagaré del vendedor represente una parte significativa de una transacción multimillonaria—, contratar a un investigador privado para la verificación de antecedentes es una precaución legítima y, en ocasiones, esencial. Un investigador experimentado puede descubrir litigios no declarados, insolvencias previas, irregularidades de identidad o antecedentes penales que podrían no aparecer en una verificación de crédito estándar. El costo de una investigación profesional es insignificante en comparación con el riesgo de financiar una operación millonaria de juegos en línea para una contraparte que incumple sus obligaciones en un plazo de dieciocho meses.

4. Establecer una tasa de interés justa en su pagaré de vendedor

Para determinar el tipo de interés adecuado para un pagaré de venta en el sector del iGaming, es fundamental comprender un principio básico: el tipo de interés refleja el riesgo, no los tipos de mercado vigentes. Durante la última década, los tipos de interés de los pagarés de venta en las adquisiciones empresariales se han mantenido en un rango constante de entre el 6 % y el 8 % anual, y este rango se aplica igualmente a las transacciones de iGaming, con una tendencia a menudo hacia los tipos más altos debido a la complejidad regulatoria del sector y la volatilidad de los ingresos.

Los compradores a veces argumentan que las tasas deberían seguir el ritmo de las hipotecas residenciales o los rendimientos de los bonos soberanos. Esto es una falsa equivalencia. Cuando un banco recupera una vivienda tras el impago de una hipoteca, recupera un activo tangible y valorado de forma independiente. En cambio, cuando se incumple el pago de un préstamo hipotecario en la adquisición de un casino en línea, lo que el vendedor suele recuperar es un negocio en dificultades: posiblemente en pleno proceso de cambio de marca, enfrentando una revisión de licencia, con una base de datos de jugadores reducida y relaciones de afiliados deterioradas. La garantía es inherentemente más débil, lo que justifica una prima de riesgo significativamente mayor.

Entre los factores clave que deben influir en la fijación de la tasa se incluyen el valor total de la empresa de juegos en línea, el perfil crediticio del comprador y su experiencia operativa en juegos en línea, el importe del pago inicial en relación con el préstamo, la estabilidad y previsibilidad de los ingresos brutos del juego (GGR) y los ingresos netos del casino (NGR) en los últimos años, y la jurisdicción de la licencia. Un casino en línea B2C estable y con licencia, que opere en un mercado europeo regulado y con ingresos netos del juego consistentes, justifica una tasa más baja que un criptocasino recién lanzado con solo seis meses de historial operativo.

5. ¿Qué porcentaje de la venta debería financiar?

No existe una respuesta universal a esta pregunta, pero la decisión debe basarse en un análisis del flujo de caja. El servicio de la deuda mensual del pagaré del vendedor debe estar cubierto cómodamente por el flujo de caja operativo del negocio, con un margen suficiente para que el comprador pueda operar el casino, financiar bonos y promociones, pagar las tarifas de la plataforma y las licencias, y percibir un ingreso operativo razonable.

Una regla práctica útil: el pago mensual del préstamo no debe superar un tercio del beneficio neto mensual promedio de la empresa. Si el activo de iGaming genera 150 000 € mensuales de beneficio neto derivado de los ingresos netos por juegos, un pago mensual de 50 000 € o menos constituye un límite razonable. Superar este umbral aumenta drásticamente el riesgo de impago y coloca a ambas partes en una situación difícil.

Basándonos en datos agregados de miles de de venta de empresas , se aplican los siguientes parámetros de referencia:

Para las pequeñas empresas de juegos en línea (sitios de afiliados, casinos de marca blanca o casas de apuestas deportivas especializadas), los vendedores suelen financiar entre el 30 % y el 50 % del precio de compra. En las transacciones de casinos en línea de tamaño mediano, en el rango de 2 a 15 millones de euros, lo habitual son pagarés del vendedor del 10 % al 20 %, y el resto se financia mediante una combinación de capital del comprador y, en algunos casos, deuda de terceros.

6. Plazo, amortización y viabilidad del flujo de caja

La mayoría de los pagarés de los vendedores en las transacciones de fusiones y adquisiciones de juegos en línea se estructuran con un plazo de amortización de entre tres y siete años, siendo cinco años el promedio del sector. El plazo tiene un impacto más significativo en las obligaciones de pago mensuales que el tipo de interés, por lo que los vendedores deberían simular diversos escenarios antes de decidirse por una estructura.

La amortización se refiere simplemente al proceso de pago del capital y los intereses en cuotas periódicas iguales durante la vigencia del préstamo. En los primeros meses de amortización, la mayor parte de cada pago se destina al pago de intereses; a medida que el saldo disminuye, una proporción cada vez mayor de cada pago reduce el capital.

Consideremos un ejemplo simplificado: un casino en línea se adquiere por 3.000.000 € con un pago inicial de 1.000.000 €. El vendedor financia los 2.000.000 € restantes al 7% durante cinco años. El pago mensual resultante es de aproximadamente 39.600 €. El servicio de la deuda anual asciende a unos 475.000 €. Si el casino genera 600.000 € de beneficio operativo neto anual, la estructura funciona: el comprador paga la deuda, cubre los gastos operativos y conserva un margen significativo. Si se reduce el plazo a dos años, el pago anual se dispara a más de 260.000 € al mes, una carga insostenible para la mayoría de las empresas de juegos en línea de ese tamaño.

La lección es sencilla: ajuste el plazo del préstamo a la capacidad real de generación de efectivo del activo e incluya un margen de seguridad para los inevitables períodos de gastos promocionales, costes de renovación de licencias o actualizaciones de plataforma a los que se enfrentan habitualmente los operadores de juegos en línea.

7. Utilización de un administrador de préstamos externo

Una vez acordado y documentado el pagaré del vendedor, recomendamos encarecidamente designar a un administrador de préstamos independiente para gestionar los pagos mensuales. Un gestor de préstamos profesional se encarga de todas las funciones de cobro, abono y desembolso, lo que elimina la carga operativa para el vendedor y reduce la posibilidad de disputas entre comprador y vendedor sobre los plazos de pago, el cálculo de intereses o la conciliación de saldos.

En el contexto del iGaming, mantener un registro financiero preciso de todos los pagos de pagarés es fundamental. Los operadores en jurisdicciones reguladas deben mantener una documentación financiera meticulosa para cumplir con los requisitos de licencia, y un administrador externo proporciona un registro de auditoría independiente que puede resultar valioso en caso de disputa o si el pagaré se asigna posteriormente a un inversor.

8. Contratos de arrendamiento y de plataforma: lo que los vendedores deben conservar

En las fusiones y adquisiciones tradicionales, generalmente se recomienda a los vendedores que mantengan el contrato de arrendamiento comercial durante la vigencia del pagaré, lo que garantiza que, en caso de impago por parte del comprador, puedan retomar la gestión del negocio sin perder las instalaciones. El equivalente de este principio en el sector del iGaming es de vital importancia, aunque las particularidades difieren del comercio minorista físico.

En las adquisiciones de casinos en línea, los acuerdos relevantes no son los contratos de arrendamiento físico, sino los acuerdos sobre la plataforma de juego, las relaciones de procesamiento de pagos y, sobre todo, la licencia de juego regulatoria. Si el comprador incumple el pago del préstamo al vendedor durante la operación, este último necesita derechos contractuales claros para retomar el control de la estructura operativa. Esto puede implicar mantener un rol operativo discreto o la condición de cofirmante en el acuerdo de la plataforma durante el período de vigencia del préstamo, o incluir derechos explícitos de intervención en el contrato de compraventa.

La licencia de juego es el aspecto más complejo. En muchas jurisdicciones —Malta, Gibraltar, Isla de Man, Curazao— las licencias se emiten a entidades legales específicas y no son transferibles automáticamente. Los vendedores deben trabajar con asesores legales especializados en iGaming para estructurar derechos de subrogación que sean comercialmente viables y cumplan con la normativa vigente. En CasinosBroker.com, ponemos en contacto a nuestros clientes con abogados especializados en iGaming precisamente para este fin.

9. Vender su pagaré si necesita liquidez

Los pagarés del vendedor no son irrevocablemente ilíquidos. Una vez que un pagaré ha madurado —normalmente después de seis a doce meses de pagos puntuales y constantes— existe un mercado de inversores especializados y compradores de pagarés que lo adquirirán, lo que proporciona al vendedor una suma global de dinero en efectivo.

La contrapartida es el descuento. Los compradores de pagarés valoran los pagarés de los vendedores de iGaming en función de la solvencia del negocio subyacente, el historial de pagos, el plazo restante y la garantía. En la venta de un pagaré, se suele recibir entre el 70 % y el 85 % del saldo pendiente, un descuento significativo, pero una vía de salida legítima si las necesidades de liquidez cambian tras el cierre.

Si prevé que en algún momento desee vender su pagaré, asegúrese desde el primer día de que esté redactado explícitamente para permitir su cesión y transferencia a terceros. Un pagaré que no sea transferible por sus términos no puede venderse, independientemente del buen desempeño del comprador.

10. Cuándo y cómo promocionar la financiación del vendedor en tu anuncio de iGaming

Decidir si anunciar de forma proactiva la financiación del vendedor en el listado de tus activos de iGaming, o mantenerla como una baza en la negociación, depende en gran medida del tamaño de la transacción y del perfil de tu comprador objetivo.

Para activos de iGaming más pequeños (sitios web de afiliados, operaciones de marca blanca o sitios de tragamonedas independientes que generen menos de 500 000 € al año), recomendamos anunciar desde el principio las condiciones específicas de financiación del vendedor en su anuncio de CasinosBroker.com. Los compradores de activos pequeños son muy sensibles a los requisitos de capital. Saber que la financiación del vendedor está disponible amplía significativamente su grupo de compradores cualificados e indica que usted es un vendedor preparado y motivado que se ha esforzado por concretar la operación.

En las transacciones de casinos online de gama media, es más común anunciarlas sin especificar condiciones de financiación, dejando la estructura del acuerdo para la fase de negociación. En este caso, una simple nota en el anuncio que indique que "las condiciones de financiación son negociables" mantiene la flexibilidad sin comprometerte con una estructura específica. Además, deja la puerta abierta a los compradores que requieren la participación del vendedor para completar su capital, sin disuadir a los compradores que pagan al contado y que podrían asumir que el vendedor necesita financiar la operación.

Si prefiere una salida en efectivo íntegra, pero consideraría la financiación para un comprador excepcionalmente cualificado —uno con un historial operativo probado en el sector del juego online, un balance sólido y relaciones regulatorias existentes—, entonces indicar que "hay financiación disponible para compradores cualificados" es una forma eficaz y honesta de plantearlo.

11. Documentos clave necesarios para las notas del vendedor de iGaming

Cada nota del vendedor, independientemente del tamaño de la transacción, requiere un conjunto de documentos legales debidamente redactados. Los componentes principales son:

Un pagaré es el instrumento fundamental. En él se especifican el capital, el tipo de interés, el calendario de pagos, las condiciones de incumplimiento, las penalizaciones por mora y los plazos para subsanar los retrasos. Debe ser redactado por un abogado con experiencia tanto en fusiones y adquisiciones comerciales como en transacciones de juegos de azar en línea; los pagarés genéricos a menudo no contemplan los riesgos específicos del sector que son relevantes en la adquisición de un casino.

Un acuerdo de garantía, junto con la presentación de un gravamen UCC (o su equivalente jurisdiccional en la UE), establece la posición de acreedor garantizado del vendedor sobre los activos del negocio. Este gravamen impide que el comprador venda, pignore o grave de cualquier otra forma el negocio de iGaming o sus activos sin el consentimiento del vendedor durante el período del pagaré; una protección fundamental dada la rapidez con la que se pueden transferir o reestructurar los activos de iGaming.

Una garantía personal de los directivos de la entidad compradora añade una capa adicional de protección, especialmente en operaciones donde el comprador es una sociedad holding o una sociedad instrumental. Los vendedores no deben considerar la solicitud de una garantía personal como una táctica agresiva; es una práctica comercial habitual y cualquier comprador experimentado comprenderá la razón.

Finalmente, el contrato de compraventa debe incluir cláusulas detalladas posteriores al cierre que especifiquen los estándares operativos mínimos: límites mínimos de ingresos netos de explotación (NGR), mantenimiento del capital circulante, obligaciones de renovación de licencias y periodicidad de los informes. Estas cláusulas constituyen un sistema de alerta temprana y una herramienta de presión contractual en caso de que el negocio comience a deteriorarse tras el cierre.

12. Preguntas frecuentes

P1. ¿Es común la financiación por parte del vendedor en las adquisiciones de casinos en línea?

Sí, es la estructura de transacción predominante para los activos de iGaming más pequeños y un componente importante de la mayoría de las transacciones de casinos medianos. Los datos del sector sugieren que más del 80 % de las ventas de pequeñas empresas incluyen algún tipo de financiación por parte del vendedor, y el sector del iGaming refleja en gran medida esta tendencia dada la dificultad de obtener financiación bancaria tradicional para activos relacionados con casinos.

P2. ¿Qué tasa de interés debería cobrar un vendedor en un pagaré de vendedor de iGaming?

El rango estándar es del 6% al 8% anual, determinado principalmente por el riesgo más que por las tasas de mercado vigentes. Factores como el perfil crediticio del comprador, el monto del pago inicial, la jurisdicción de la licencia, la estabilidad de los ingresos brutos del gobierno y la estructura general de la transacción influyen en el precio que el vendedor debería fijar para el pagaré, ya sea dentro de ese rango o, en ocasiones, por encima.

P3. ¿Cuál debería ser el plazo de un pagaré del vendedor para la adquisición de un casino?

El plazo habitual oscila entre tres y siete años, siendo cinco el más común. El factor clave es la viabilidad del flujo de caja: el servicio de la deuda mensual debe estar cubierto cómodamente por el flujo de caja operativo neto del casino, con un margen suficiente para que el comprador pueda operar y expandir el negocio.

P4. ¿Qué sucede si el comprador incumple el pago del vendedor?

El pagaré debe contener cláusulas explícitas de incumplimiento, incluyendo plazos de subsanación, cláusulas de aceleración y recursos legales. Junto con un gravamen sobre los activos de la empresa, conforme al Código Comercial Uniforme (UCC) o equivalente, el vendedor puede intentar recuperar el activo de iGaming o solicitar la ejecución judicial del saldo pendiente. La calidad de su documentación legal determina la solidez de su posición en caso de incumplimiento.

P5. ¿Puedo ofrecer financiación al vendedor en un casino en línea con licencia sin poner en riesgo la licencia?

Las implicaciones en materia de licencias dependen exclusivamente de la jurisdicción y de los términos específicos del acuerdo. En la mayoría de los mercados regulados, la licencia permanece en manos de la entidad operadora, y la financiación del vendedor no constituye, por sí sola, un cambio de control. Sin embargo, si el pagaré incluye derechos de intervención o cláusulas de influencia operativa, podría ser necesaria una notificación o aprobación de la licencia. Siempre consulte con un asesor legal especializado en juegos en línea antes de finalizar la estructura.

P6. ¿Debo exigir una garantía personal al comprador?

Para los compradores individuales, una garantía personal, además de la garantía de los activos de la empresa, es práctica habitual y muy recomendable. Para los compradores corporativos, las garantías de los directivos de la entidad adquirente cumplen la misma función. Esto añade una capa significativa de protección y garantiza que el interés financiero personal del comprador esté involucrado, y no solo el capital de la entidad adquirente.

P7. ¿De cuánto debería ser el pago inicial en una operación de compraventa de juegos en línea?

Recomendamos un pago inicial mínimo del 30%, e idealmente del 50%, del precio de compra acordado. Un pago inicial mayor reduce significativamente el riesgo de impago y demuestra el compromiso real del comprador con la adquisición. Los pagos iniciales inferiores al 30% deben tratarse con mucha precaución, ya que los compradores con un riesgo mínimo tienen estadísticamente más probabilidades de abandonar un negocio en dificultades en lugar de afrontar los problemas operativos.

P8. ¿Puedo vender mi pagaré a un tercero si necesito efectivo después del cierre?

Sí, siempre y cuando el pagaré esté redactado explícitamente para permitir la cesión. Tras un periodo de prueba de seis a doce meses —que demuestre pagos puntuales y constantes— existe un mercado de inversores especializados en pagarés que comprarán el saldo restante, generalmente con un descuento del 15 % al 30 %. Asegúrese de que la transferibilidad esté contemplada en el pagaré desde el primer día si desea conservar esta posibilidad.

P9. ¿Qué indicadores financieros debo exigir al comprador que mantenga después del cierre de la operación?

En el contexto del iGaming, las cláusulas contractuales posteriores al cierre podrían incluir umbrales mínimos mensuales de ingresos brutos de juego (NGR o GGR), niveles mínimos de capital de trabajo, el mantenimiento vigente de las licencias de juego, la prohibición de realizar cambios sustanciales en el proveedor de la plataforma o la infraestructura de procesamiento de pagos sin el consentimiento del vendedor, y la obligación de presentar informes financieros trimestrales. Estas cláusulas sirven tanto como sistema de alerta temprana como de palanca contractual en caso de deterioro del negocio.

P10. ¿Cómo ayuda CasinosBroker.com a estructurar la financiación del vendedor en las operaciones de iGaming?

CasinosBroker.com ofrece asesoramiento integral en fusiones y adquisiciones para transacciones de activos de iGaming, incluyendo la estructuración de acuerdos, valoración, estructura de pagarés del vendedor, apoyo para la calificación del comprador y acceso a abogados especializados en iGaming. Nuestros asesores cuentan con amplia experiencia en adquisiciones de casinos online, transacciones de sitios afiliados y acuerdos de plataformas de marca blanca, y comprenden los matices regulatorios y comerciales específicos que distinguen las fusiones y adquisiciones en iGaming de la intermediación comercial convencional. Tanto si es un comprador que busca estructurar una adquisición eficiente en capital como si es un vendedor que desea maximizar el valor de salida, somos su socio especializado.

Conclusión: Cómo lograr que la financiación del vendedor funcione en tu operación de iGaming

La financiación por parte del vendedor no es señal de desesperación ni una solución de último recurso para los compradores que no pueden obtener capital. En la industria del iGaming, es un mecanismo de transacción sofisticado y ampliamente adoptado que beneficia a ambas partes: permite a los vendedores alcanzar valoraciones más altas y salidas fiscalmente eficientes, al tiempo que ofrece a los compradores una vía práctica para adquirir activos de casinos en línea regulados sin la carga imposible de un pago en efectivo completo.

La clave del éxito reside en la preparación: términos claros, documentación legal sólida, una exhaustiva cualificación del comprador y una proyección realista del flujo de caja basada en la economía real del activo de iGaming objeto de la transacción. Los vendedores que abordan la financiación con la mentalidad de un prestamista disciplinado —y no de un vendedor motivado y desesperado por cerrar la operación— estructurarán acuerdos sólidos que generarán los beneficios previstos.

Si está considerando la venta o adquisición de un casino en línea, un negocio de afiliados de juegos de azar, una plataforma de iGaming de marca blanca o cualquier otro activo relacionado con los juegos digitales, CasinosBroker.com es la plataforma especializada y el mercado creado precisamente para este tipo de transacciones. Explore nuestros listados actuales, contacte con nuestro equipo de asesores o envíe su activo para una valoración confidencial; permítanos ayudarle a estructurar la operación que mejor se adapte a su estrategia de salida o adquisición.

información sobre licencias y novedades en fusiones y adquisiciones, directamente en tu feed.