What Every Online Casino Buyer and Seller Needs to Know

Executive Summary

When it comes to buying or selling an online casino, an iGaming affiliate site, or any digital gaming asset, few metrics generate more initial discussion than Return on Investment (ROI). ROI in iGaming is the percentage return earned on a given amount of capital deployed, straightforward to compute, and powerful precisely because of that simplicity. For example: a €100,000 return on a €1,000,000 investment equals a 10% ROI. In the context of iGaming M&A, this quick calculation enables buyers to compare the potential returns across different acquisition targets, from established online casinos and crypto gambling platforms to white-label operations and slot game studios, before committing to deeper due diligence.

CasinosBroker’s iGaming business valuation service applies these frameworks to real assets — providing operators with an accurate, market-calibrated exit value based on 110+ closed transactions across affiliate sites, white label casinos, and full company mandates.

That said, experienced iGaming acquirers quickly learn that ROI is a starting point, not a destination. It does not account for deal leverage, time horizons, capital appreciation, or the unique qualitative advantages that iGaming businesses offer. This guide, produced by the advisory team at CasinosBroker.com, explores every dimension of ROI as it applies to iGaming acquisitions: how to calculate it correctly, what it misses, and how to use it intelligently alongside other valuation metrics.

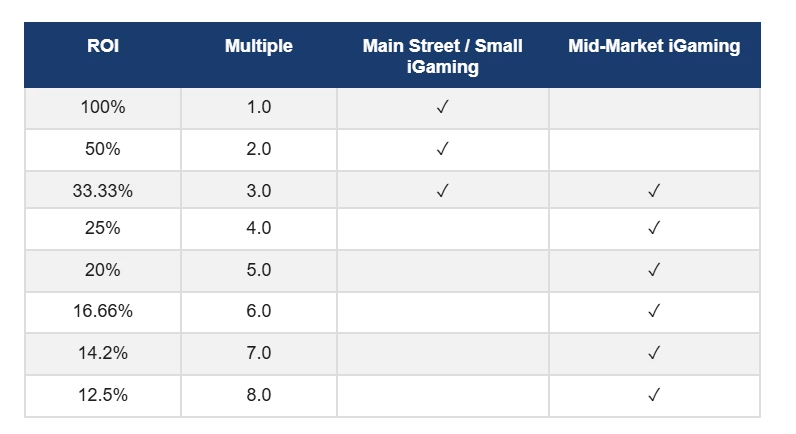

2. Typical ROI Benchmarks in iGaming

In iGaming M&A, ROI is effectively the inverse of the valuation multiple applied to a business’s earnings. If a mid-sized online casino is acquired at a 4.0× EBITDA multiple, the implied ROI is 25%. Understanding this relationship gives both buyers and sellers a fast way to sanity-check pricing during initial conversations.

The table below translates common iGaming valuation multiples into their corresponding ROI figures, segmented by business scale:

To benchmark your specific asset against current market comparables, browse our active iGaming listings — including asking prices and asset metrics across affiliate sites, white label casinos, and full company acquisitions.

In practice, smaller iGaming businesses, independent slot sites, niche sports betting operations, or single-jurisdiction online casinos, typically trade in the 2.0×–4.0× range (50%–25% ROI). Mid-market platforms with proven GGR track records, scalable infrastructure, and licensed operations in Tier-1 jurisdictions such as Malta (MGA), Gibraltar, or the Isle of Man tend to command 4.0×–7.0× EBITDA (25%–14% ROI). Premium assets with proprietary technology, strong player databases, and recurring bonus infrastructure may push beyond these norms.

3. What Is the Purpose of Calculating ROI?

3.1 Comparing iGaming Investments

The primary utility of ROI in iGaming M&A is cross-investment comparison. When you are evaluating multiple acquisition targets simultaneously, say, a crypto casino against a regulated affiliate network, you need a metric that normalises returns across very different asset types and price points. ROI provides that common denominator in seconds.

A buyer considering a €2,000,000 online casino generating €200,000 in EBITDA immediately recognises a 10% ROI. That number can be weighed against alternative iGaming investments, established sportsbooks, or even passive real estate, helping the buyer decide whether to proceed with deeper analysis or move on.

3.2 ROI as a Quick Deal Filter

Experienced iGaming M&A advisors and private equity groups that are active in the digital gaming space use ROI as a first-pass filter. Before commissioning a full financial audit, reviewing player traffic data, or assessing a platform’s bonus mechanics, a skilled acquirer will calculate a back-of-envelope ROI to determine whether the asking price reflects fair value. This is not a definitive answer, it is a prompt: is this conversation worth continuing?

3.3 ROI as a Rule of Thumb

Like most rules of thumb in business, ROI trades precision for speed. It is inherently crude, much like using a thumb to estimate a length rather than a tape measure. The real skill lies in knowing when the ROI is sufficient to make a decision and when you need to reach for more sophisticated tools like IRR or DCF. In high-velocity deal environments, iGaming conferences, bilateral LP meetings, or informal broker calls, being able to calculate and articulate returns in real-time is a professional currency of its own.

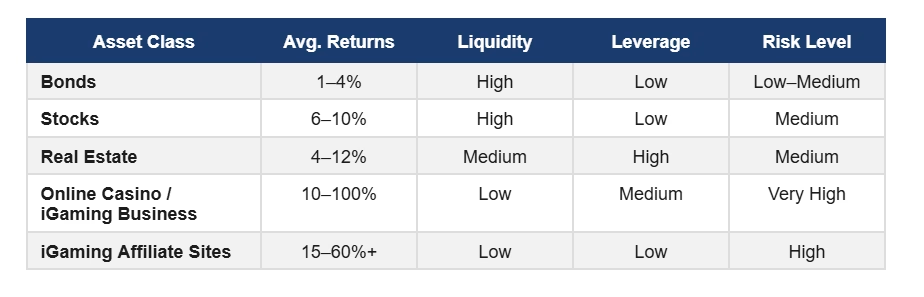

4. ROI Across Asset Classes: Where Does iGaming Sit?

Online casinos and iGaming assets occupy a distinctive position among investable asset classes. They offer the potential for exceptional returns, but they come with a risk profile that reflects the regulatory complexity, player churn dynamics, and platform dependency inherent in the sector. The table below contextualises iGaming returns against other common investment vehicles:

The wide ROI range for iGaming businesses, from roughly 10% at the low end to well over 100% for distressed or fast-scaling assets, reflects the enormous diversity of the sector. A dormant crypto casino with an expired Curaçao licence selling for below net asset value is a very different proposition to a growing MGA-licensed platform with 50,000 active players and a proprietary loyalty engine.

5. Advantages and Disadvantages of Using ROI in iGaming

Advantages

The near-universal adoption of ROI across finance, private equity, and now digital assets makes it the common language of investment comparison. It is fast to compute, requires no specialist software, and can be communicated clearly to both technical operators and financial buyers who may be entering the iGaming space for the first time. For a CasinosBroker advisor working through a pipeline of 20 acquisition candidates, the ability to rank each by implied ROI in under a minute is genuinely valuable.

Disadvantages

The limitations of ROI are significant enough to warrant careful attention. First, it is time-agnostic, a 30% ROI achieved in two years is not the same as a 30% ROI achieved in eight years, yet the raw figure looks identical. Second, it ignores the effect of leverage: an acquisition financed with 75% debt will produce a dramatically different cash-on-cash return than the same deal done with 100% equity, even if the headline ROI appears equivalent. Third, in iGaming specifically, ROI as typically calculated captures only current-year cash flows, completely ignoring platform scalability, player lifetime value growth, or regulatory expansion opportunities that represent the majority of value in high-growth digital gaming businesses. Finally, ROI says nothing about risk, comparing a casino with stable GGR from a grey-market jurisdiction to one with an MGA licence and diversified payment processing is an apples-to-oranges exercise if evaluated by ROI alone.

6. Is Buying an Online Casino Really an Investment?

This question is more consequential in iGaming than in almost any other industry. The classic definition of an investment involves deploying capital in exchange for financial returns, without necessarily requiring the investor’s personal labour. Many acquisitions in the online casino and affiliate space blur this distinction significantly.

An operator who buys a small online casino and then personally manages CRM campaigns, monitors payment processing, handles VIP players, and liaises with software providers is not primarily an investor, they are a working owner. In this case, the buyer’s own salary must be deducted from SDE before a meaningful ROI calculation is possible. The lost opportunity cost, what the buyer could earn in an equivalent role elsewhere, is the correct benchmark, not an abstract market salary.

Consider this example: if you are acquiring a boutique online casino for €600,000 and the business generates €200,000 in SDE, the headline ROI is 33%. But if operating this casino requires your full-time involvement, and your relevant market salary as a Head of Casino or iGaming Product Director is €90,000, the true EBITDA is €110,000, producing an ROI closer to 18%. The difference is material.

Based on €250,000 SDE × 3.0 Multiple, Effect of Owner Salary on ROI:

| The ROI on an online casino acquisition is inherently buyer-specific. Two acquirers looking at the same deal, one a strategic operator, the other a passive PE investor, will arrive at completely different return profiles. |

7. What ROI Fails to Capture in iGaming

7.1 The Value of Operator Freedom and Optionality

One of the most undervalued aspects of owning an online casino or iGaming affiliate business is freedom, the ability to make product decisions, pivot to new verticals like live casino or sports betting, or expand into emerging crypto gambling markets without seeking approval from a corporate hierarchy. For many iGaming entrepreneurs, this strategic autonomy carries real economic value that no ROI formula can quantify. Building a casino brand that compounds player loyalty, deepens affiliate relationships, and expands jurisdiction by jurisdiction creates options that simply do not exist in passive investment vehicles.

7.2 Capital Appreciation and Multiple Expansion in iGaming

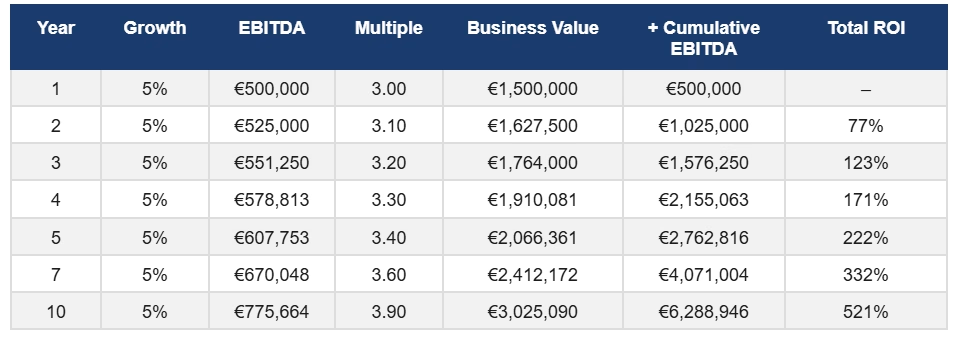

Perhaps the most significant blind spot of ROI in the iGaming sector is its failure to account for capital appreciation. When an online casino grows its net gaming revenue (NGR), the business value does not merely grow in proportion, the applicable valuation multiple often expands simultaneously, multiplying the effect. A platform that grows EBITDA from €500,000 to €775,000 over five years at a 5% annual rate, while also seeing its multiple expand from 3.0× to 3.9×, nearly doubles in enterprise value. Include the cumulative operating cash flows retained over that period, and the total ROI far exceeds the annual yield alone.

Scenario A: 5% Annual EBITDA Growth with Multiple Expansion

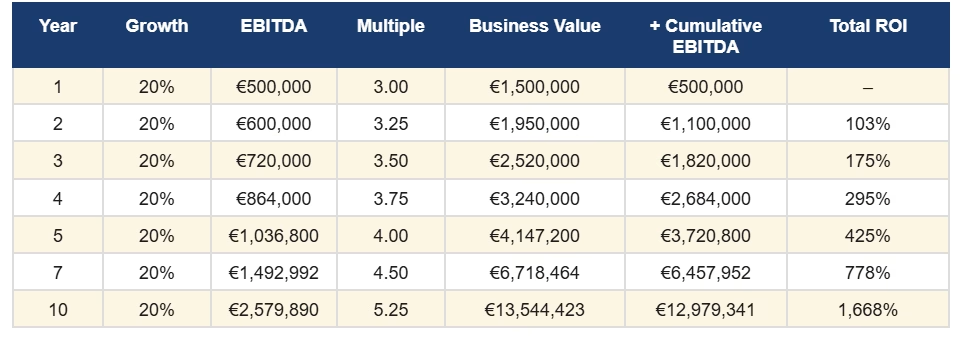

Scenario B: 20% Annual EBITDA Growth (High-Growth iGaming Platform)

Scenario B: 20% Annual EBITDA Growth (High-Growth iGaming Platform)

A 20% sustained growth rate is exceptional and will not continue indefinitely, but it is not unheard of in fast-scaling online casino groups entering new regulated markets or launching high-conversion crypto casino verticals. The compounding effect on total ROI, when cumulative EBITDA and capital appreciation are combined, is dramatic, and entirely invisible to a buyer who evaluates only today’s return.

7.3 The Impact of Time: Annualised Returns

ROI is blind to time. A 50% return generated in one year is fundamentally different from a 50% return generated over a decade, yet both report identically. In iGaming M&A, where integration timelines, licence transfer periods, and platform migration cycles can consume one to two years before an acquirer sees normalised returns, time-agnostic metrics are dangerously misleading. When comparing two acquisition targets, always annualise your ROI or, for more complex deal structures, calculate IRR to understand the velocity of return, not just its magnitude.

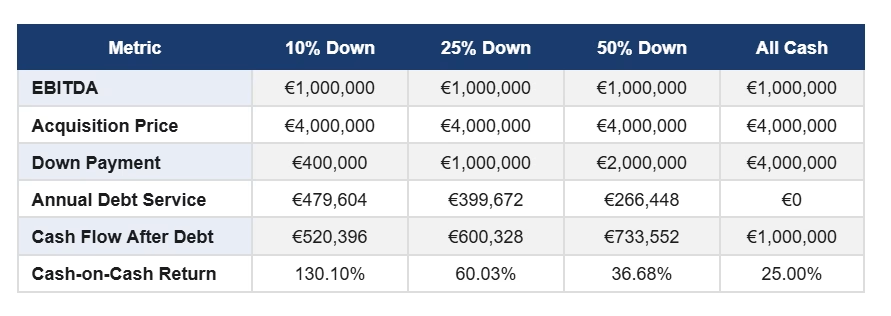

7.4 The Impact of Leverage: Cash-on-Cash Return

Leverage dramatically alters the real returns available to iGaming acquirers who finance part of the acquisition through seller financing, revenue-based earnouts, or external debt. The tables below model a €4,000,000 online casino acquisition at various leverage points, assuming a 10-year repayment at 6% interest:

The data makes a compelling case for intelligent use of leverage in iGaming acquisitions: a buyer who contributes only 10% equity and finances the balance can generate a cash-on-cash return in excess of 130%, compared to 25% for an all-cash buyer. Of course, this amplification works in both directions, declining GGR or unexpected regulatory action can quickly turn a highly leveraged deal into a distressed situation. The key is to stress-test cash flow projections against realistic downside scenarios before committing to a debt structure.

8. SDE vs. EBITDA: Which to Use for iGaming Valuations?

The choice between Seller’s Discretionary Earnings (SDE) and EBITDA is one of the most consequential methodological decisions in iGaming business valuation. The distinction is simple: SDE adds back the owner’s total compensation to net income, while EBITDA treats management as a replaceable function at market rates. The right choice depends entirely on the buyer’s profile and the operational structure of the target.

For smaller online casino operations, single-brand affiliates, or white-label casinos where the founding operator is central to platform management, player relations, and supplier negotiations, SDE is the appropriate measure. The buyer will likely assume these functions and should account for their own labour in the return calculation. For larger platforms with dedicated management teams, where the CEO, Head of Operations, and CRM Director would all continue post-acquisition, EBITDA is the correct basis, and the multiple applied will be higher, reflecting the reduced execution risk for the buyer.

| Line Item | SDE | EBITDA | Notes |

| Net Income | €500,000 | €500,000 | Starting point is the same |

| Owner’s Salary | €200,000 (included) | Not included | Key distinction |

| Total Cash Flow | €700,000 | €500,000 | SDE = higher apparent ROI |

| Typical Multiple Used | 2×–4× | 3×–7× | Higher multiple for EBITDA businesses |

| Best Used For | Small iGaming ops | Mid-market acquisitions | Applies to online casinos & affiliates |

Applying the wrong metric can significantly distort an iGaming acquisition’s apparent attractiveness. A small affiliate site whose operator personally builds SEO content, manages link-building campaigns, and handles advertiser relationships will look far more profitable under SDE than under EBITDA, but that SDE figure disappears the moment the current owner exits. Buyers must always interrogate what happens to earnings when management changes hands.

9. Practical Tips for Using ROI in iGaming M&A

The following principles, drawn from CasinosBroker’s advisory experience across hundreds of iGaming transactions, will help buyers and sellers use ROI intelligently rather than naively.

Verify the cash flow figure first. No ROI calculation is more reliable than the EBITDA or SDE number it rests upon. In iGaming, owners frequently adjust for non-recurring marketing spend, platform migration costs, or one-off bonus liabilities. Understand exactly what has been included and excluded. Request the underlying GGR, NGR, and operational cost breakdown before accepting any stated earnings figure.

Clarify whether you are buying an investment or an operator role. If the target casino requires your active daily involvement in compliance, payments, and player acquisition, deduct your relevant market salary before calculating ROI. Failing to do so produces an inflated return that evaporates the moment you account for your own time.

Run the leverage scenario. Before committing to an all-cash offer, model the deal with 25%, 50%, and 75% financing. Understand how annual debt service affects your free cash flow and what GGR decline percentage would push you into negative territory. iGaming businesses are subject to sudden regulatory changes, payment processor exits, and player churn events that can compress EBITDA quickly.

Build in capital appreciation assumptions. If the business has a credible growth trajectory, expanding into new jurisdictions, launching live casino or sports betting verticals, or deploying AI-driven player retention tools, model the appreciation in enterprise value over a 3-5 year horizon. Compare the total return (capital gain plus cumulative cash flow) to the initial investment, not just the year-one income yield.

Compare across asset classes. An iGaming acquisition at a 20% ROI competes with many other uses of capital. Evaluate it against regulated real estate, diversified equity portfolios, and other digital businesses, adjusting for the materially higher risk and the non-financial upside of brand building in the gaming sector.

10. Alternatives to ROI for iGaming Valuations

Cash-on-Cash Return (Return on Equity)

Cash-on-cash return is essential whenever leverage is part of the deal structure, which in iGaming M&A often means seller financing, earnout mechanics, or bridge lending from specialist iGaming lenders. This metric measures the actual cash received relative to the cash actually deployed, stripping out the distortion introduced by debt. For acquisitions involving a revenue-based earnout component, cash-on-cash return gives a far cleaner picture of first-year financial performance than raw ROI.

Internal Rate of Return (IRR)

IRR is the most comprehensive return metric available and is standard practice among private equity groups active in iGaming acquisitions. It accounts for the timing of every cash flow, initial investment, annual distributions, and eventual exit proceeds, and expresses them as a single annualised return figure. Its principal drawback is complexity: IRR requires projected cash flows across the full hold period, meaning assumptions about GGR growth, regulatory stability, and exit multiples all feed directly into the output. For acquisitions above €2,000,000 in enterprise value, IRR modelling is a minimum standard of analytical rigour.

Real Rate of Return

In jurisdictions with significant monetary inflation, relevant for buyers acquiring iGaming assets in emerging markets or paying in currencies subject to exchange rate volatility, the real rate of return adjusts nominal returns for inflation. While less commonly used in core European iGaming transactions, it becomes critical when evaluating assets in LatAm, Eastern European, or certain Asian markets.

Discounted Cash Flow (DCF)

For high-growth iGaming platforms, particularly proprietary slot studios, data-driven affiliate networks, or AI-powered retention platforms, DCF analysis is the most theoretically sound valuation method. It values a business based on the present value of its projected future cash flows, explicitly incorporating growth rate assumptions, discount rates, and terminal value estimates. DCF is particularly appropriate where current EBITDA understates long-term value due to heavy investment in platform development or market expansion.

11. Frequently Asked Questions

Q1: What is a good ROI for buying an online casino?

A ‘good’ ROI depends heavily on the buyer’s profile and the deal structure. Broadly, an online casino generating a 25–33% ROI at acquisition (equivalent to a 3.0×–4.0× EBITDA multiple) is considered fair value for a mid-sized regulated platform. Smaller operations or those in grey-market jurisdictions may offer higher headline ROIs (40–50%+), but this typically reflects elevated operational or regulatory risk. Strategic buyers, those who can unlock synergies through shared infrastructure, existing player databases, or cross-selling, may accept lower initial ROIs in exchange for capital appreciation.

Q2: What EBITDA multiple is typical for online casino acquisitions?

Mid-market online casino acquisitions in regulated jurisdictions such as Malta (MGA), Gibraltar, or the UK (UKGC) typically transact in the 4.0×–7.0× EBITDA range. Smaller, owner-operated casinos often trade closer to 2.0×–4.0× SDE. Premium assets, those with proprietary technology, multi-jurisdiction licensing, and consistent GGR growth, have historically commanded 8.0×–12.0× EBITDA, particularly when acquired by large gaming conglomerates or listed operators. CasinosBroker tracks live transaction data across our marketplace to provide up-to-date benchmarks for specific asset categories.

Q3: Should I use SDE or EBITDA to value an iGaming affiliate business?

For iGaming affiliate businesses where the owner is personally responsible for content production, SEO strategy, or relationship management, SDE is the appropriate metric, it captures the full economic benefit available to an owner-operator. If the affiliate business is managed by a dedicated team that will continue post-acquisition, EBITDA is more appropriate. The key test is simple: what happens to earnings if the current owner exits on day one? If earnings decline materially, SDE is inflated by the owner’s embedded labour and should be adjusted before calculating ROI.

Q4: How does leverage affect the ROI on an online casino acquisition?

Leverage amplifies returns dramatically. An acquisition financed with only 10% equity can produce a cash-on-cash return exceeding 130%, compared to 25% for an all-cash buyer of the same asset at the same EBITDA multiple. This is why seller financing and earnout structures are attractive to sophisticated iGaming buyers. However, leverage also amplifies downside risk, any shortfall in GGR or regulatory disruption (licence suspension, payment processor withdrawal) reduces the cash available for debt service. Always model your leveraged return against a 20–30% GGR downside scenario before committing.

Q5: What ROI can I expect from buying an iGaming affiliate site?

iGaming affiliate acquisitions span a wide return range depending on traffic quality, niche (casino, slots, sports betting, crypto gambling), and jurisdiction targeting. Established affiliate sites with stable organic search traffic and diversified operator partnerships typically trade at 2.5×–5.0× annual net revenue or EBITDA, implying ROIs of 20–40%. Sites with concentrated traffic risk (single keyword dependency, single operator revenue) should be discounted accordingly. The best affiliate acquisitions are those where the buyer can actively grow organic rankings, expand into new GEOs, or add previously un-monetised content.

Q6: How does regulatory risk affect iGaming business valuation and ROI?

Regulatory risk is one of the most significant value drivers, and destroyers, in iGaming M&A. A casino operating under a robust, transferable licence from the MGA, UKGC, or Swedish Spelinspektionen commands a material valuation premium over an equivalent platform operating under a Curaçao or Anjouan licence, precisely because regulatory stability reduces the discount rate applied to future cash flows. From an ROI perspective, a regulated platform may appear to offer a lower initial yield, but it carries significantly lower risk of overnight revenue loss due to licence action, banking withdrawal, or market re-regulation.

Q7: What is capital appreciation in the context of buying an online casino?

Capital appreciation refers to the increase in the enterprise value of an online casino or iGaming business over time. In iGaming, appreciation is driven by two factors: EBITDA growth (as the business generates more net gaming revenue) and multiple expansion (as the business becomes more scalable, regulated, or profitable, the market applies a higher valuation multiple to each unit of EBITDA). A buyer who acquires a casino at 3.0× EBITDA and sells five years later at 5.0× EBITDA on a higher earnings base can generate total returns many times larger than the initial annual yield suggested.

Q8: Can I use ROI to compare buying a crypto casino versus a traditional online casino?

ROI provides a useful first-pass comparison, but the underlying risk profiles are different enough that raw ROI comparisons require adjustment. Crypto casinos often offer higher headline ROIs due to lower payment processing costs, pseudonymous operations, and rapid customer acquisition in unregulated or lightly regulated jurisdictions. However, they typically carry higher regulatory tail risk, more volatile GGR (correlated with cryptocurrency price movements), and lower enterprise value stability. A crypto casino at 40% ROI and a regulated online casino at 22% ROI are not directly comparable without adjusting for risk, time horizon, and jurisdiction exposure.

Q9: What alternatives to ROI should iGaming buyers use when evaluating acquisitions?

For acquisitions above €1,000,000 in enterprise value, CasinosBroker recommends supplementing ROI with at minimum: (1) cash-on-cash return to model the effect of deal financing, (2) annualised ROI to account for integration timelines, and (3) a simplified 5-year capital appreciation scenario assuming conservative GGR growth. For larger or more complex transactions, multi-licence platforms, studio acquisitions, or white-label infrastructure deals, a full IRR model and DCF sensitivity analysis are the appropriate standard.

Q10: How does CasinosBroker help buyers and sellers determine ROI on iGaming assets?

CasinosBroker.com operates as a specialist iGaming M&A brokerage and marketplace (marketplace.casinosbroker.com), providing buyers and sellers with access to vetted acquisition opportunities, comparable transaction data, and advisory support through the full deal lifecycle. Our advisors work with sellers to produce financial normalisation analyses that accurately reflect SDE and EBITDA, and with buyers to model acquisition ROI under multiple scenarios. Whether you are acquiring your first online casino, selling a mature affiliate network, or evaluating a white-label platform investment, our team can help you move from back-of-envelope ROI to fully diligenced investment conviction.

12. Conclusion: ROI Is a Starting Point, Not a Strategy

Return on Investment is a powerful tool in the iGaming M&A toolkit, fast, universal, and intuitive. Used correctly, it allows buyers to rank acquisition targets in seconds and sellers to frame their asking price in terms investors immediately understand. But experienced operators and institutional acquirers in the online casino, affiliate, and iGaming infrastructure space know that ROI is only the beginning of the conversation.

The true return on an iGaming acquisition emerges from the intersection of initial yield, capital appreciation driven by GGR growth and multiple expansion, intelligent deal financing, and the strategic optionality that comes from owning a scalable digital gaming asset in a growing regulated market. A 20% year-one ROI on a platform with a credible path to 5× growth, an MGA licence, and a proprietary retention engine is a far superior opportunity to a 35% ROI on a static, single-jurisdiction grey-market operation.

At CasinosBroker.com, we work with buyers and sellers across the full spectrum of iGaming assets, from independent slot sites and crypto casinos to mid-market sportsbooks and white-label platforms, to ensure that every valuation is grounded in real transaction data and industry-specific expertise. If you are exploring an acquisition or considering bringing your iGaming business to market, our advisory team is available to provide a complimentary valuation discussion.

Whether you are buying or selling an iGaming business, accurate valuation is the foundation of every successful transaction. Explore our seller advisory services or browse current acquisition opportunities to see how current market pricing compares to the ROI benchmarks in this guide.

| Ready to explore iGaming acquisition opportunities or get a professional valuation of your online casino or affiliate business? Visit marketplace.casinosbroker.com to browse current listings, or contact our M&A advisory team directly to discuss your objectives in confidence. |

licensing insights, and M&A deal flow — straight to your feed.