Executive Summary

In the world of iGaming mergers and acquisitions, buyer and seller rarely see eye to eye on valuation. The seller — whether exiting an online casino, a sportsbook platform, or a white-label gaming operation — naturally wants top dollar. The buyer, on the other hand, may be skeptical about whether projected GGR targets will materialize, whether licensed player bases will be retained post-acquisition, or whether a key affiliate network will survive the ownership change. This tension is universal in iGaming M&A, and the instrument that most consistently bridges it is the earnout.

An earnout is a deferred payment mechanism by which the buyer agrees to pay the seller an additional sum contingent on the acquired iGaming business meeting predetermined performance targets after closing. It is one of the most powerful and most misunderstood tools in the iGaming deal structuring toolkit. At CasinosBroker, we work with online casino operators, platform providers, affiliate businesses, and investors across dozens of jurisdictions — and earnouts come up in virtually every mid-market transaction we handle.

This guide will walk you through everything you need to know about earnouts in iGaming M&A: what they are, how they are structured, when they should and should not be used, how they are documented, and what practical steps buyers and sellers can take to protect their interests throughout the process.

What Is an Earnout in iGaming M&A?

At its most fundamental level, an earnout is a form of contingent, deferred consideration paid from the buyer to the seller after the closing of an iGaming transaction. Unlike a fixed seller’s note — where a predetermined repayment schedule is agreed in advance — an earnout ties payment to the future performance of the acquired business. The seller only receives the earnout if specific targets are met within an agreed-upon period, typically one to five years post-closing.

In the iGaming sector, earnout metrics can be tied to Gross Gaming Revenue (GGR), Net Gaming Revenue (NGR), EBITDA, active player counts, regulatory licensing milestones, retention of affiliate partnerships, or even the successful launch of a new market vertical such as live dealer or sports betting. The key principle is that a good earnout metric is objective, clearly defined, and resistant to manipulation by either party.

Earnouts are relatively rare in smaller iGaming transactions — where asset values fall under €2–3 million — but they are a standard feature of mid-market iGaming deals, where CasinosBroker operates most actively. In larger iGaming M&A deals involving publicly traded gaming groups, stock-for-stock structures often serve a similar economic purpose. For privately held online casinos, sportsbooks, gaming platforms, and affiliate businesses transacting in the €5M–€50M range, earnouts are one of the most important negotiating instruments available.

The Two Types of Earnouts

Incentivization Earnouts

Incentive-based earnouts are deployed when both buyer and seller broadly agree on the current valuation of the iGaming business, but the buyer wants to motivate the seller — often the founding operator or CEO — to remain engaged and drive growth post-acquisition. In this structure, the earnout does not bridge a price gap; it functions as performance-linked upside compensation for the seller who continues to manage the business.

This is particularly common in online casino and affiliate iGaming acquisitions where the business is heavily dependent on the original operator’s relationships — with payment providers, regulators, key affiliates, or player communities. Private equity buyers in the iGaming space routinely structure 10% to 25% of total purchase price as an incentivization earnout, ensuring the seller remains invested in the outcome of the acquisition.

Risk Mitigation Earnouts

Risk-mitigation earnouts, by contrast, exist to protect the buyer from paying for value that may not materialize. They are used to bridge genuine disagreements about the future prospects of the iGaming business — for example, when a casino’s GGR is heavily concentrated in one or two markets facing regulatory shifts, or when a sportsbook’s revenue is tied to a handful of major affiliate partners whose continuation post-closing is uncertain.

In this category, the earnout directly reduces the buyer’s financial risk by making a portion of the purchase price contingent on outcomes. If the risks materialize negatively, the buyer has not overpaid. If they do not, the seller is rewarded accordingly. This creates a rational, if complex, framework for resolving iGaming valuation disputes.

Advantages of Earnouts in iGaming Transactions

Bridging Valuation Gaps in Online Casino Deals

The most compelling advantage of earnouts in iGaming M&A is their unique ability to bridge valuation gaps between buyers and sellers. When an online casino operator claims their business is on an accelerating GGR trajectory — perhaps entering a newly regulated market or launching a revamped live casino vertical — but has not yet demonstrated that performance in audited financials, the buyer faces a dilemma. Paying full price for projected growth is risky; offering only current-earnings multiples may kill the deal.

An earnout solves this problem elegantly. The buyer pays a base price reflective of verified current performance and agrees to pay additional consideration if the projected GGR or EBITDA materializes within the earnout period. The seller gets the opportunity to receive the full valuation they believe the business deserves. Neither party has to compromise on their fundamental view of the business — they simply defer resolution to the market.

Managing iGaming-Specific Uncertainty

The iGaming industry carries layers of uncertainty that most other sectors do not. Regulatory changes — a license being revoked, a new market opening, a payment processing restriction — can dramatically alter revenue trajectories overnight. Player retention metrics can shift significantly following platform migrations or brand redesigns. Affiliate marketing partnerships, which drive a disproportionate share of player acquisition for many online casinos, can dissolve or downgrade without warning.

Earnouts provide a structured mechanism for managing exactly this type of uncertainty. Rather than demanding that buyers guess correctly about how a regulatory development or platform migration will play out, earnouts allow the parties to share that risk rationally. The seller bears some of the uncertainty by accepting contingent consideration; the buyer bears the remainder by paying a fair base price.

Alignment Between Operators and Acquirers

In the iGaming sector, where founder-operators often have deep personal relationships with their player communities, affiliate networks, and payment providers, post-acquisition continuity is not merely desirable — it is often essential to protecting deal value. An earnout creates powerful alignment: the seller remains economically motivated to cooperate fully in the transition, facilitate warm introductions, and maintain operational quality because their compensation depends on it. This is especially relevant in iGaming businesses where the founding operator is the primary relationship-holder with key third parties.

Disadvantages and Risks of Earnouts

Manipulation Risks in iGaming Earnouts

The iGaming context introduces some particularly acute manipulation risks that are worth calling out explicitly. If an earnout is tied to GGR or NGR, a buyer who subsequently gains control of the iGaming platform can redirect affiliate traffic to other brands within their portfolio, reducing revenue attributable to the acquired business. They can also adjust bonus structures or promotional spend in ways that depress net revenue for earnout calculation purposes — practices that are difficult to monitor and even harder to litigate.

Conversely, a seller who retains operational control during the earnout period may pursue aggressive short-term player acquisition strategies — high bonus offers, loosened wagering requirements, or aggressive affiliate commission structures — that inflate short-term GGR at the expense of player lifetime value and long-term sustainability. This is the classic earnout short-termism problem, and it is particularly dangerous in iGaming where such levers are readily available and their effects are not always immediately visible in the financial statements.

Earnouts tied to top-line revenue metrics such as GGR are generally more difficult to manipulate than those tied to net earnings or EBITDA. However, no iGaming earnout is completely immune to creative accounting or operational manipulation by a sufficiently motivated counterparty.

Disputes, Complexity, and Integration Challenges

Earnouts are, by their nature, adversarial structures. The buyer has a financial incentive to minimize earnout payments; the seller has an incentive to maximize them. Even where both parties act in complete good faith, differing interpretations of accounting definitions — how NGR is calculated, whether certain bonus costs are deducted before or after the earnout threshold, how chargebacks are treated — can generate significant disputes. In the iGaming sector, where revenue accounting can be genuinely complex due to jurisdictional variations in taxation and reporting standards, this problem is amplified.

Post-closing integration is also materially complicated by earnouts. If the acquired online casino is being merged into a larger platform or rebranded as part of a portfolio strategy, independently measuring the earnout target becomes increasingly difficult. Buyers who wish to pursue integration-driven synergies — consolidating payment processing, shared back-office, combined affiliate programs — may find that an earnout prevents them from doing so, limiting the very value they sought to create through acquisition. This is one of the most significant structural tensions in iGaming M&A involving earnouts, and CasinosBroker advises clients to address it explicitly at the LOI stage.

How to Determine the Right Earnout Amount

Determining an appropriate earnout quantum begins with a rigorous preliminary valuation of the iGaming business — one that accounts for not just current GGR and EBITDA, but also the specific risk factors inherent in the business: regulatory exposure, customer concentration, affiliate dependency, licensing jurisdiction, and technology platform stability.

Once a valuation range is established, the earnout is calibrated against the specific risks and uncertainties that separate the bottom and top of that range. If the primary uncertainty is whether a newly regulated market entry will succeed, the earnout is sized to reflect the incremental value of that market materializing versus not. If the uncertainty is whether a key affiliate partnership will be renewed post-closing, the earnout reflects the revenue contribution of that partnership.

A practical benchmark for mid-market iGaming transactions is that earnouts typically represent 10% to 25% of total enterprise value, though they can be as high as 75% in early-stage iGaming businesses with substantial projected but unproven growth. The seller should always approach earnout negotiations with a clear-eyed assessment of the probability of achieving each target — and should ideally be prepared, financially and emotionally, to receive nothing from the earnout. If the base purchase price is insufficient without the earnout, the seller’s negotiating position is fundamentally compromised.

Documenting iGaming Earnouts: LOI to Purchase Agreement

Earnouts are documented at two critical stages in the iGaming M&A transaction timeline.

At the Letter of Intent (LOI) stage, buyers often propose earnout structures in broad strokes as they begin to identify the key risks in the iGaming business. This is also where sellers make one of their most consequential mistakes: accepting vague earnout language in the LOI — such as “an earnout of up to €5 million with targets to be agreed during due diligence” — in order to preserve deal momentum. This approach invariably weakens the seller’s position, since by the time the purchase agreement is drafted, the buyer has completed due diligence and may have identified additional risks to justify more restrictive earnout terms.

CasinosBroker consistently advises iGaming sellers to insist on specific, fully defined earnout terms at the LOI stage: the total earnout quantum, the specific metrics (GGR, NGR, EBITDA, player counts), the measurement period, the threshold and cap structure, the calculation methodology, and the dispute resolution mechanism. The seller’s negotiating leverage is at its maximum before the LOI is signed — and dissipates rapidly thereafter.

At the Purchase Agreement stage, the earnout is documented in exhaustive detail, typically in a standalone earnout schedule or agreement that forms part of the broader transaction documents. This is where experienced M&A legal counsel — specifically counsel with iGaming industry expertise — is essential. Ambiguous language regarding how GGR is calculated, whether specific bonus types are included or excluded, how multi-currency revenues are converted, or how the earnout interacts with indemnification obligations can cost sellers hundreds of thousands of euros in disputed payments.

Factors That Affect Earnout Prevalence in iGaming

Several macro and industry-specific factors determine how commonly earnouts appear in iGaming M&A transactions at any given time.

Market conditions play a significant role. In a seller’s market — when iGaming asset valuations are elevated, strategic buyers are competing aggressively, and capital is abundant — sellers can typically command higher upfront cash consideration with minimal or no earnout component. In a buyer’s market, by contrast, earnouts become more prevalent as buyers seek downside protection and sellers have fewer competing offers.

The regulatory environment of the target business is also highly determinative. iGaming businesses operating under licenses in highly regulated, stable jurisdictions — such as the UK, Malta, or Gibraltar — typically attract cleaner deal structures with less earnout dependency. Businesses with licenses in emerging or less stable regulatory jurisdictions, or those in the process of applying for new licenses, are far more likely to involve earnouts tied to regulatory milestones.

The type of buyer matters considerably as well. Private equity acquirers in the iGaming space are generally more comfortable with earnout structures than individual operators or strategic corporate buyers. PE firms have the legal and financial infrastructure to draft, monitor, and enforce complex earnout provisions — and they frequently use incentivization earnouts to retain founders in the business post-acquisition. Individual buyers, who are often acquiring their first or second iGaming asset, typically prefer simpler deal structures with higher upfront cash and minimal earnout complexity.

iGaming Deal Structures with Earnouts

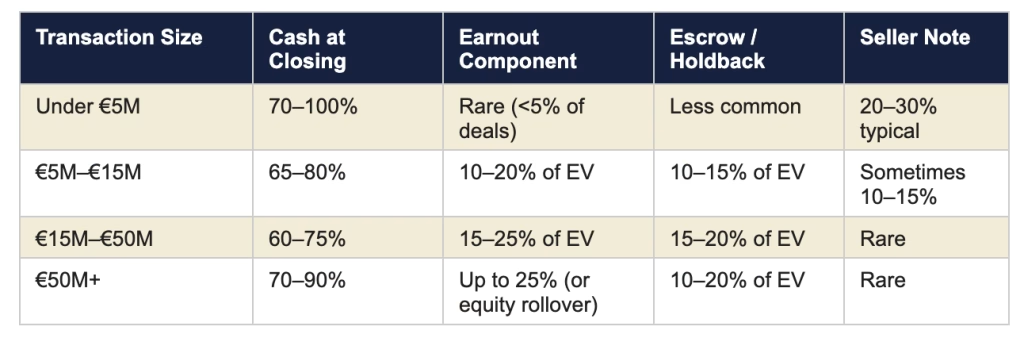

Smaller Transactions: Under €5M

For smaller iGaming acquisitions — white-label casino operations, niche affiliate websites, smaller regulated gaming licenses — the deal structure is typically straightforward. Cash at closing represents 70% to 100% of total consideration, sometimes supplemented by a seller’s note with a three-to-five-year repayment schedule. Earnouts are rare at this level, primarily because the legal and advisory costs of drafting a robust earnout agreement can be disproportionate to the transaction size, and because buyers at this level typically lack the institutional sophistication to manage earnout monitoring and enforcement.

The most common deal structure at this size involves 70–80% cash at closing, with the remainder structured as a seller note subordinated to any bank or SBA-equivalent financing. Regulatory approval timelines often affect closing mechanics but do not usually trigger earnout structures.

Mid-Market Transactions: €5M–€50M

This is the core transaction range where CasinosBroker operates and where earnouts are most commonly deployed in iGaming M&A. At this level — covering regulated online casinos, licensed sportsbooks, established affiliate networks, and gaming platform providers — deal structures are genuinely complex and earnouts are a standard feature of the negotiation.

Cash typically represents 60% to 80% of total transaction value at closing, with earnouts and escrows accounting for the remaining 20% to 40%. Earnouts in this range generally represent 10% to 25% of enterprise value, though they can be higher in businesses with particularly uncertain growth trajectories. Escrows of 10% to 20% of purchase price are common to cover reps and warranties indemnification claims for the first 12 to 24 months post-closing.

Typical iGaming Earnout Deal Structure Table

Primary Objectives of an Earnout

Primary Objectives of an Earnout

Bridging the Valuation Gap

The most cited purpose of an earnout in iGaming M&A is to bridge the gap between what a buyer is willing to pay based on current, verified performance and what a seller believes the business is worth based on anticipated future performance. This is not a failure of negotiation — it is a rational response to genuine uncertainty. When a buyer and seller cannot agree on the value of an iGaming business today, an earnout allows them to let the business’s actual performance over the next one to three years adjudicate the question.

Addressing Uncertainty

Without an earnout, the only mechanism for managing uncertainty is a reduced purchase price — which penalizes the seller even if the uncertain scenario ultimately plays out favorably. Earnouts allow both parties to share the risk of uncertainty proportionately, rather than placing the entire burden on one side of the transaction.

Aligning Interests Post-Closing

In iGaming acquisitions where the founding operator remains involved post-closing — whether as CEO, brand ambassador, or strategic advisor — the earnout creates a powerful alignment mechanism. The seller’s ongoing compensation is tied directly to the performance outcomes the buyer cares most about: player retention, GGR growth, successful market expansion, or the onboarding of key affiliate partners. This alignment reduces the risk of a disengaged founder and increases the probability that the acquisition achieves its strategic objectives.

iGaming-Specific Earnout Scenarios

Player Base and Customer Retention Risk

Customer concentration is one of the most significant risk factors in iGaming M&A. An online casino that generates 40% of its GGR from a single VIP player segment — or that relies on a proprietary player database acquired under a specific licensing arrangement — faces genuine retention uncertainty post-acquisition. A well-structured earnout in this context might tie a portion of the purchase price to the verified retention of the top player cohorts at the 90, 180, and 360-day marks following closing. CasinosBroker has structured several such earnouts for clients, and they can be effective when the measurement methodology is clearly defined upfront.

Licensing and Regulatory Milestones

Many iGaming businesses are acquired at a stage when a licensing application is pending — in a new jurisdiction, or for a new product vertical such as sports betting or live dealer. In these cases, the buyer may be willing to pay a premium for the anticipated license but unwilling to pay that premium before the license is actually issued. An earnout tied to the successful issuance of the license — with clear timelines and objective criteria — is a rational solution. However, CasinosBroker cautions that earnouts should not substitute for regulatory due diligence. If the licensing application has material deficiencies, no earnout structure resolves that underlying risk.

Key Affiliate and Tech Partner Risk

The affiliate marketing ecosystem is the lifeblood of player acquisition for most online casinos and sportsbooks. An iGaming business that generates 60% of its new player volume through a single tier-one affiliate partner faces significant post-acquisition risk if that relationship depends on the original operator’s personal credibility or bespoke commercial terms. An earnout that ties a portion of the purchase price to the verified continuation of top affiliate partnerships through a post-closing period — measured by affiliate-attributed player registration volumes — is one of the more sophisticated but effective structures CasinosBroker has seen implemented in iGaming M&A.

When Earnouts Should NOT Be Used

Despite their flexibility, earnouts are not a universal solution to iGaming valuation challenges. There are specific circumstances in which CasinosBroker advises clients strongly against deploying an earnout structure.

Earnouts should not be used as a substitute for proper iGaming business valuation. If a buyer proposes a deeply discounted base price on the grounds that an earnout will compensate the seller for the full value — essentially deferring the entire valuation question to a contingent future event — this is a structurally unfair arrangement that the seller should resist. The base purchase price should always reflect the verified current fair market value of the iGaming business. The earnout should compensate for specific, identifiable risks and opportunities beyond that baseline — not for general operational uncertainty that any business owner faces.

Earnouts are also ill-suited to iGaming transactions where deep operational integration is planned immediately post-closing. If the buyer intends to migrate the acquired casino to a new platform, rebrand it under a different domain, and consolidate its affiliate program with an existing portfolio — all within six months of closing — measuring earnout performance independently becomes practically impossible. In these cases, CasinosBroker typically recommends either a clean cash transaction at a negotiated price, or an equity rollover structure where the seller retains a meaningful minority stake in the combined business.

Prerequisites Before Agreeing to an Earnout

Before agreeing to an earnout in an iGaming transaction, several critical prerequisites should be in place. Most importantly, the seller should receive sufficient cash at closing — independent of any earnout — to meet their financial objectives. The earnout should be treated psychologically and financially as a potential bonus, not as a critical component of the seller’s retirement or reinvestment capital. Sellers who are financially dependent on receiving the earnout are placed in a structurally weak position throughout the earnout period.

Trust between buyer and seller is paramount. Even the most meticulously drafted iGaming earnout agreement cannot fully compensate for a counterparty who is determined to minimize payments through creative operational management. CasinosBroker consistently emphasizes that earnout success correlates more strongly with the quality of the buyer-seller relationship than with the sophistication of the legal drafting — though the latter certainly matters.

The seller should also perform thorough due diligence on the buyer: their track record in iGaming acquisitions, their operational capabilities, their financial resources, and their reputation within the industry. Speaking with founders of businesses previously acquired by the buyer — a reasonable request that serious buyers should readily grant — can reveal patterns in how earnout disputes are handled.

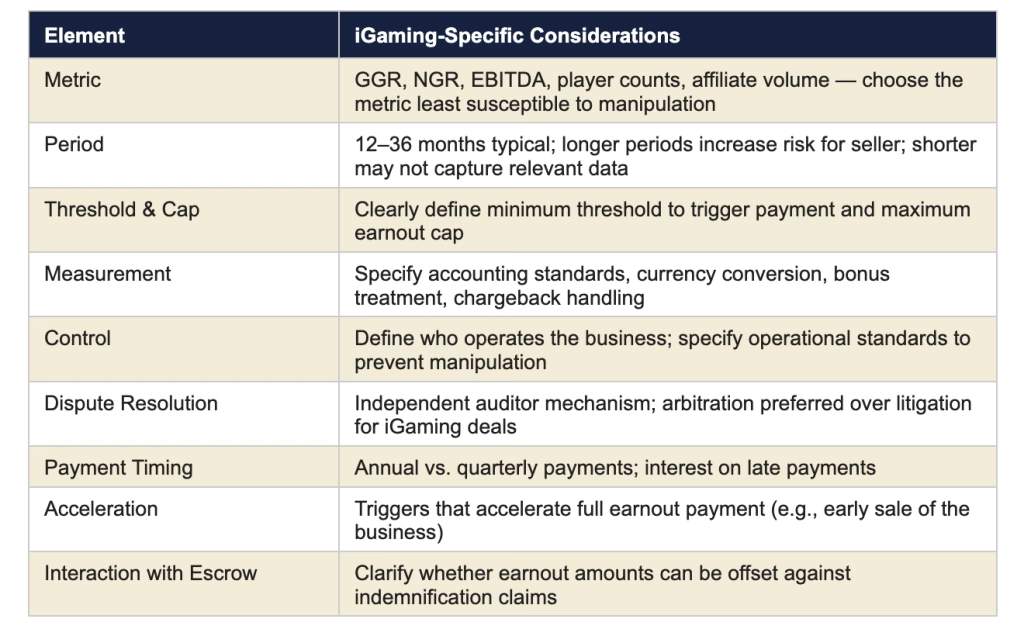

Key Elements of a Well-Drafted iGaming Earnout

Frequently Asked Questions (FAQ)

Frequently Asked Questions (FAQ)

- What is an earnout in the context of buying or selling an online casino?

An earnout is a form of deferred, contingent consideration in an iGaming M&A transaction. The buyer agrees to pay the seller an additional sum — beyond the upfront cash at closing — provided the acquired online casino, sportsbook, or gaming platform meets specific performance targets within a defined post-closing period. These targets are typically tied to revenue metrics such as GGR or NGR, EBITDA, or operational milestones like regulatory licensing or player retention benchmarks.

- How common are earnouts in iGaming M&A transactions?

Earnouts are relatively rare in smaller iGaming asset sales (under €2–3M) but are a standard feature of mid-market iGaming deals in the €5M–€50M range. CasinosBroker sees earnouts deployed in a significant portion of mid-market transactions, particularly those involving regulated online casinos, established sportsbooks, and gaming platform providers where valuation gaps and specific operational risks need to be addressed structurally.

- What metrics are typically used in iGaming earnouts?

The most common earnout metrics in iGaming M&A are Gross Gaming Revenue (GGR), Net Gaming Revenue (NGR), and EBITDA. Top-line revenue metrics like GGR are generally preferred because they are harder to manipulate than net earnings metrics. Non-financial metrics — such as the retention of key affiliate partnerships, the issuance of a pending gaming license, or the successful launch of a new market — are also used in iGaming-specific contexts where financial metrics alone cannot capture the relevant risk.

- How long does an iGaming earnout period typically last?

Most iGaming earnout periods range from one to three years post-closing. Shorter periods — six to twelve months — may be used for specific, binary milestones like regulatory approval. Longer periods increase uncertainty for both parties and are more susceptible to changing market conditions unrelated to the seller’s performance. CasinosBroker generally advises sellers to push for shorter, clearly defined earnout periods with well-defined metrics.

- Can the buyer manipulate an iGaming earnout to reduce payments?

Yes, earnout manipulation is a genuine risk in iGaming M&A, and the industry’s operational complexity makes it particularly acute. A buyer in control of the acquired platform can shift affiliate traffic, adjust bonus structures, alter payment processing fees, or reallocate shared costs in ways that artificially depress revenue or EBITDA for earnout calculation purposes. This is why CasinosBroker emphasizes that earnout agreements must include explicit operational standards, independent auditor mechanisms, and clear definitions for every revenue and cost line used in the calculation.

- What is the difference between an earnout and seller financing in iGaming deals?

Seller financing — typically structured as a promissory note — involves a fixed repayment schedule agreed at closing. The seller will receive that amount regardless of how the business performs, provided the buyer does not default. An earnout, by contrast, is entirely contingent on post-closing performance: the amount is variable and may be zero if targets are not met. Seller financing is more predictable and less risky for the seller; earnouts offer higher potential upside but carry significantly more uncertainty.

- How does a regulatory licensing milestone work as an earnout trigger?

In iGaming M&A transactions involving businesses with pending licensing applications, a regulatory milestone earnout ties a specified portion of the purchase price to the successful issuance of the gaming license within a defined timeframe. If the license is granted, the seller receives the contingent payment. If it is not granted within the agreed period — due to regulatory delays, application deficiencies, or market changes — the payment is not made. These structures are common in acquisitions of businesses seeking licenses in newly regulated markets.

- What happens to the earnout if the acquired iGaming business is sold again before the earnout period ends?

This is a critical issue that should be addressed explicitly in the earnout agreement. Most well-drafted iGaming earnout agreements include an acceleration clause that triggers full or partial earnout payment if the business is sold, merged, or significantly restructured before the earnout period concludes. Without this protection, a seller could find their earnout effectively extinguished by a subsequent transaction over which they have no control.

- Should the seller remain involved in the business during the earnout period?

This depends heavily on the specific deal structure and the nature of the earnout metrics. If the earnout is tied to GGR or operational performance that the seller can meaningfully influence, remaining involved — as CEO, Managing Director, or senior advisor — is generally in the seller’s interest. If the buyer intends to integrate the business rapidly into a larger platform, the seller’s ongoing involvement may have limited impact on earnout outcomes, and a cleaner exit with a higher upfront payment is often preferable.

- How does CasinosBroker approach earnouts when brokering iGaming transactions?

CasinosBroker approaches earnouts as one component within a holistic deal structuring framework. We begin with a rigorous preliminary valuation that identifies the specific risk factors and growth opportunities in the iGaming business, then assess whether an earnout is the most appropriate mechanism for addressing them — or whether alternative structures such as equity rollovers, escrow holdbacks, or adjusted purchase price multiples would serve both parties better. When earnouts are appropriate, we guide sellers through the critical task of defining earnout terms at the LOI stage — before negotiating leverage diminishes — and connect clients with experienced iGaming M&A legal counsel for the documentation phase.

Conclusion: CasinosBroker’s Perspective on Earnouts

Earnouts are among the most powerful and most mishandled instruments in iGaming M&A. When deployed correctly — with clearly defined metrics, mutually agreed accounting standards, explicit operational protections, and realistic targets — they can unlock transactions that would otherwise fail due to valuation disagreements and genuine performance uncertainty. They protect buyers from overpaying for unproven growth and reward sellers who continue to drive real value post-closing.

When deployed carelessly — with vague LOI language, poorly defined metrics, or excessive dependence on the buyer’s goodwill — earnouts become a source of post-closing conflict that can consume years of legal fees and permanently damage the professional relationships that the iGaming industry depends upon. The difference between these two outcomes lies almost entirely in the quality of preparation before the earnout terms are agreed.

At CasinosBroker, we specialize in navigating exactly this complexity. Whether you are selling a regulated online casino, acquiring a licensed sportsbook, divesting an affiliate network, or structuring a platform acquisition, our M&A advisory team has the iGaming-specific expertise to ensure that your deal structure — including any earnout component — is designed to achieve your strategic objectives, not create tomorrow’s dispute.

licensing insights, and M&A deal flow — straight to your feed.